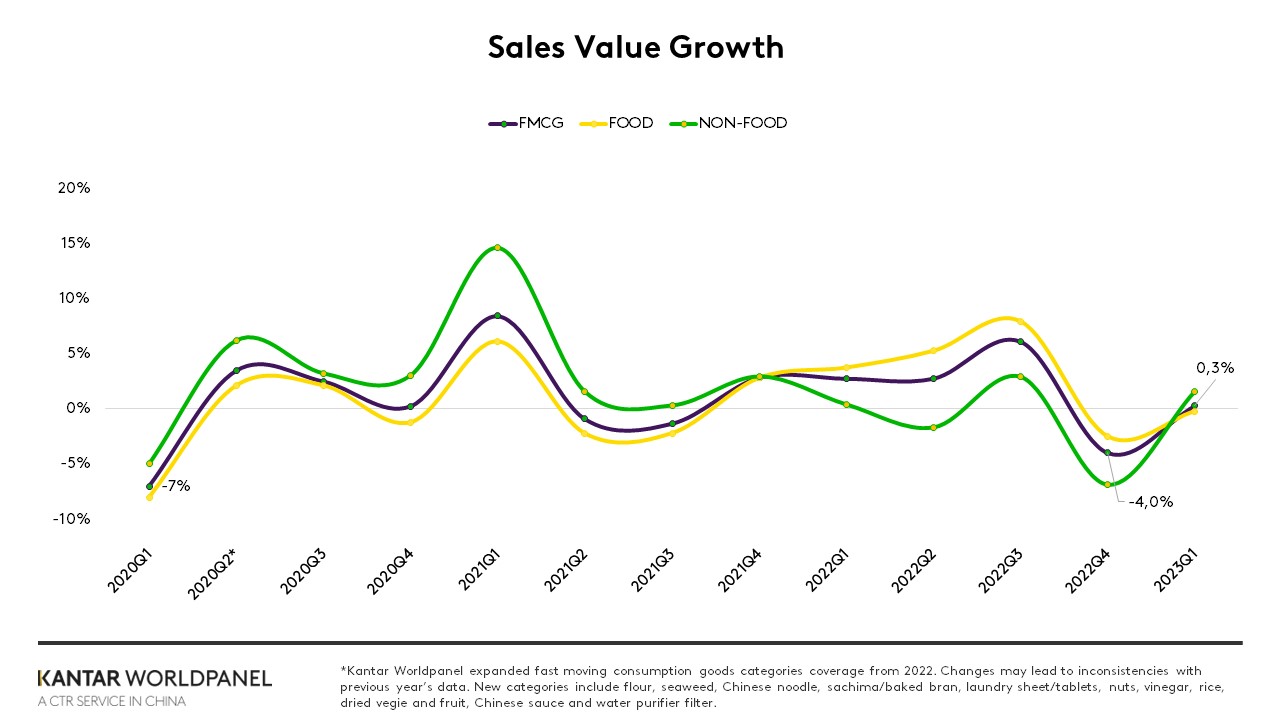

FMCG sales in urban China returned to growth in the first quarter of 2023, with a value increase of 0.3% year-on-year; 4.3% higher than the fourth quarter of 2022. Due to the steady recovery of the economy in Mainland China, consumption occasions have gradually increased, and this has been a driving force behind the growth.

As consumers' lives returned to normal, the demand for stockpiling food at home declined, and as a result, the sales growth of food and beverages in the first quarter was lower than that of household cleaning and personal care products. The household cleaning category has continued its growth momentum, with a particularly impressive performance in the sales of paper products.

Beverages returned to growth after a brief decline in the fourth quarter of 2022, with double-digit value increases recorded in juice, functional drinks, and ready-to-drink tea. Spend on ambient milk and nutritional supplements increased by 7% and 18% respectively in the first quarter, reflecting continued post-pandemic demand among Chinese consumers for products that improve their physical fitness and immunity.

Smaller supermarkets outshine larger formats

The performance of hypermarkets and large supermarkets continued to weaken in the first quarter of 2023. The ongoing decline in footfall is still the biggest challenge faced by large format retailers, with a 16.4% and 10.7% decrease for hypermarkets and large supermarkets respectively compared with the same period last year.

At the same time, sales in small supermarkets increased by 15.5% year-on-year, and purchase frequency and spend per trip both rose. Convenience stores also enjoyed an expansion of their buyer base and purchase frequency. This shows that Chinese consumers are sticking to the habit of shopping in proximity channels that they developed during the pandemic.

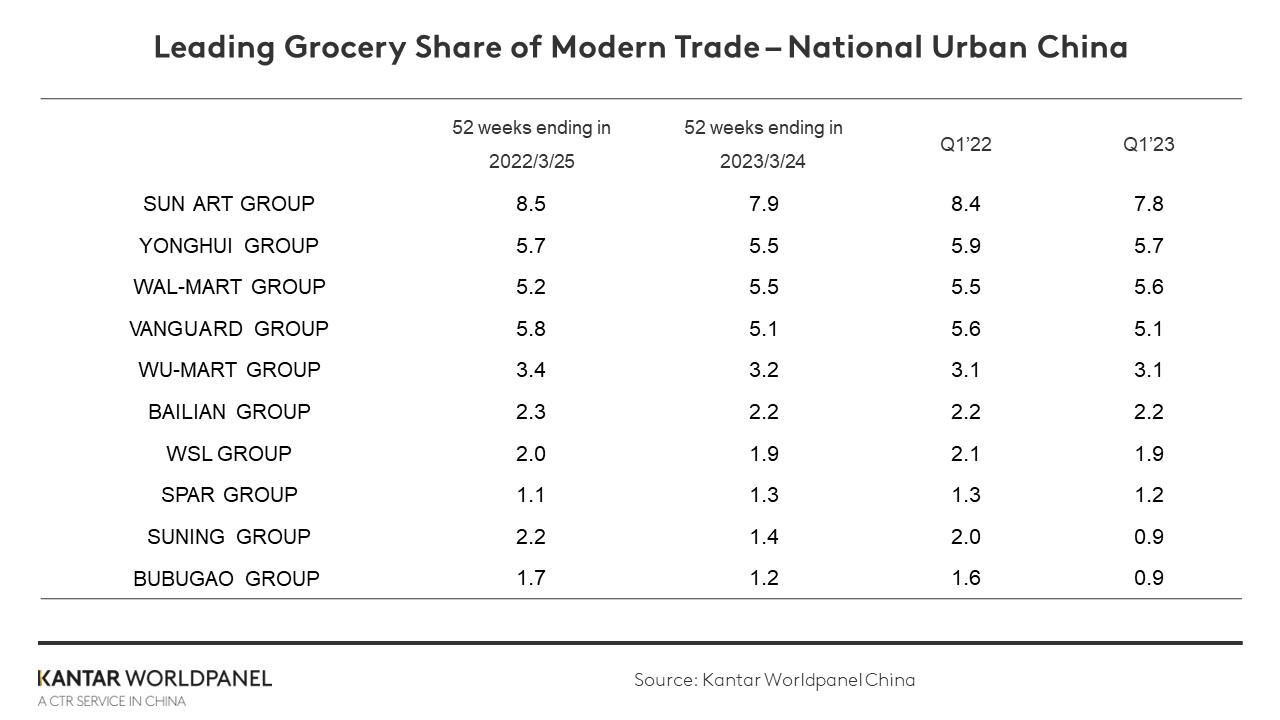

The fragmentation trend within modern trade is becoming more obvious – with the overall market share of the top 10 retailers falling to 34.5% in the first quarter from 37.7% a year earlier. Suning Group and BBG Group in particular experienced a significant drop in share.

As the key growth engine of Walmart Group, Sam’s Club’s market share within modern trade increased by 0.6%, boosting Walmart’s overall share by 0.2%.

The competition between membership stores has further intensified, and both Hema X and Metro increased their market share in the first quarter. Retailers continue to invest in product development, building private label brands, and optimising the supply chain to meet consumers' needs for quality, cost-effectiveness, and multiple experiences.

Hongqi Chain has performed especially well. Its format combines the ‘everywhere’ of convenience stores with the wide selection of categories offered by supermarkets, providing consumers with a timely and convenient shopping experience. After achieving both revenue and net profit growth last year, Hongqi’s revenue in the first quarter of 2023 increased by 4.7% year-on-year.

Interest ecommerce makes great strides

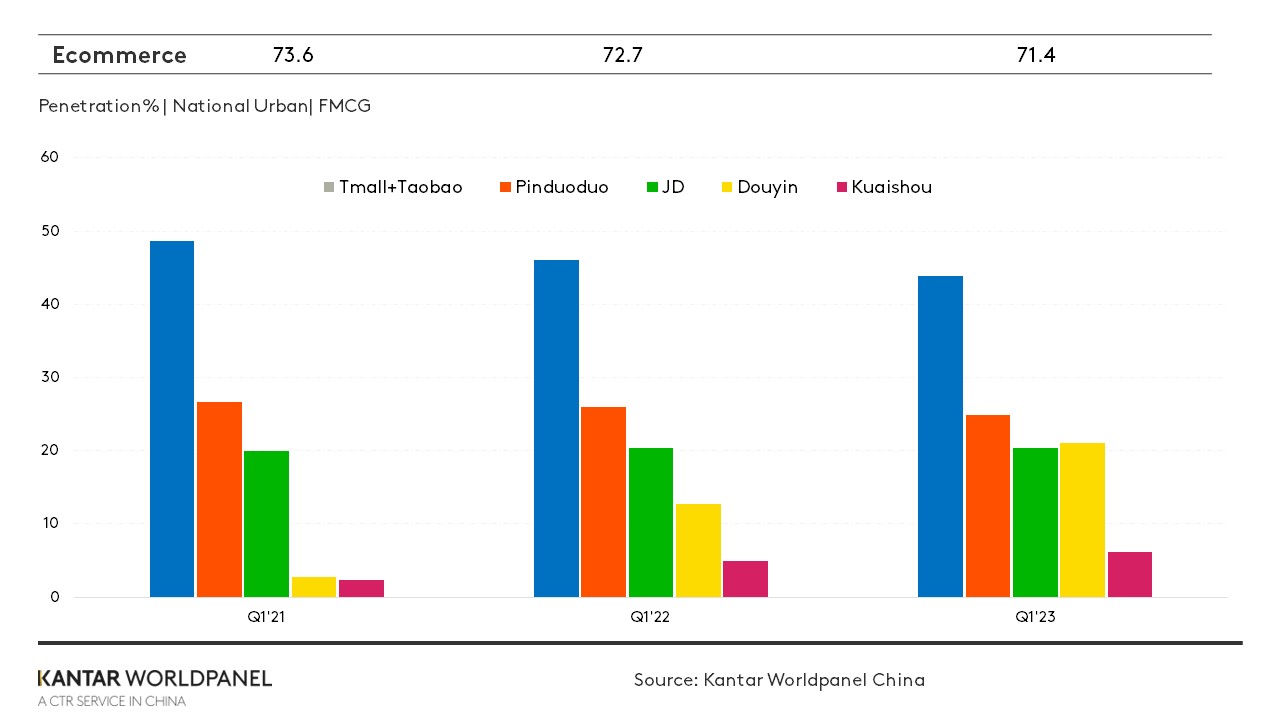

In 2022, the rise of interest ecommerce (shopping via video and streaming platforms) and the development of O2O (shopping online, with delivery from offline stores) posed a significant threat to traditional ecommerce. In the first quarter, the penetration of Alibaba, JD.com and Pinduoduo continued to decline compared with the same period last year, but the rate of loss has decelerated since China’s post-COVID reopening.

In addition, consumers’ purchase frequency has rebounded significantly.

Among the interest ecommerce platforms, Douyin and Kuaishou have maintained rapid growth. Although spend per trip has dropped slightly, they performed highly in recruiting buyers and driving frequency. In the first quarter of 2023, more than 20% of Chinese urban households purchased FMCG on Douyin.

Rapid growth in O2O sales continues

Although spend per trip has dropped slightly compared with the same period last year, purchase frequency continued to increase. More than 34% of Chinese urban households bought FMCG through O2O in the first quarter of the year.

During the pandemic, consumers had more opportunities to use O2O platforms, and gradually increased their usage. This habit has not disappeared. As consumers turn to O2O for more categories and occasions, it is expected that its growth momentum will continue.

At the same time, community group buy (CGB) platforms achieved a strong year-on-year increase in buyers during Q1. Although the economy in China has begun to recover, the purchasing power of consumers, especially low- and middle-income groups, still needs time to recoup. The appeal of the value for money that CGB offers, along with the expanding selection of categories and services, will endure.

If you would like to learn more, please get in touch with our experts or access our data visualisation tool to explore current and historical grocery market data for China.