Take-home grocery sales are expected to surpass £13 billion for the first time ever this December. Our latest figures showed that sales grew by 6.3% over the four weeks to 26 November 2023 to reach £11.7 billion.

The scene is set for record-breaking spend through the supermarket tills this Christmas. The festive period is always a bumper one for the grocers with consumers buying on average 10% more items than in a typical month. Some of the increase, of course, will also be driven by the ongoing price inflation we’ve seen this year.

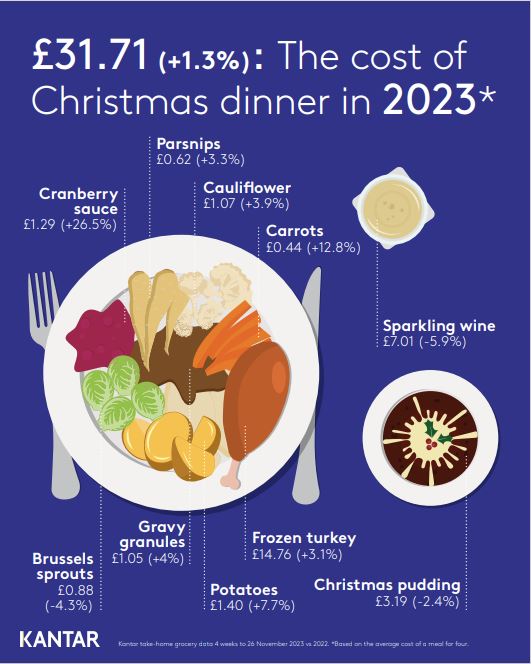

While the rate at which grocery prices are rising is still well above the norm, the good news for shoppers is that inflation is continuing to come down. It dropped again in November to 9.1%. The retailers are also battling it out to offer value to consumers during this important month for trading and are doing what they can to keep prices low. In a sign of just how fierce the contest is between the grocers, the cost of a Christmas dinner for four has risen well below the overall inflation rate this year at 1.3%, as some items on our festive plate have actually fallen in price. Brussels sprouts are now 4.3% cheaper than 12 months ago so there’s no excuse for people not to enjoy them.

Aided by promotions branded growth edges ahead of own label

Retailers are putting the emphasis on own-label lines and promotions to attract people through their doors. Kantar data shows that spending on offers hit its highest level in over two years in the latest period at 28.4%. The amount of money spent on deals usually leaps in the run up to Christmas, but this year is already looking a bit different. We’re well above 2022 levels, with customers making an additional £180 million in savings this November versus 12 months ago. Brands have benefited from the boost in offers and have now edged ahead of their own-label counterparts, growing sales by 6.5% versus 6.4% for retailer lines. However, own-label is still doing incredibly well and premium lines especially so. These products are up by 15.4% year on year, with wine, chilled ready meals and fresh beef among the big winners last month. We’re likely to see a seasonal jump in premium stuffing, sausage meat and Christmas puddings over the coming weeks.

Friday 22 December is predicted to be the single busiest day in store as people rush to make sure they have what they need ahead of the big day. Nearly 41 million brussels sprouts will pass through the tills every day in the week before 25 December.

Sainsbury's, Tesco, Lidl and Aldi all gain share

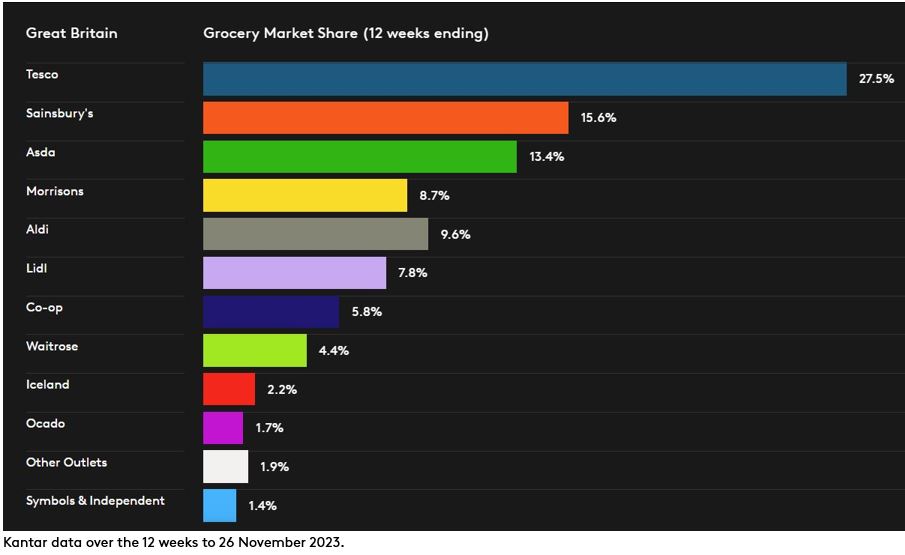

The two biggest supermarkets continued their fightback in the battle for market share last month. Sainsbury’s delivered its largest market share gain in over a decade this November, taking an additional 0.4 percentage points to reach 15.6%. The last time it made this big a jump was in March 2013. Its growth was driven in no small part by the continued success of its own-label offer, with sales of its popular ‘Taste the Difference’ range up by a whopping 23% year on year. These premium products feature prominently in Sainsbury’s Christmas TV spot this year and our testing showed its lead TV ad is one of the top performers for potential short-term sales impact.* We’ll be keeping a close eye on the numbers next month to see how this translates at the tills.

Tesco also put in a strong performance to increase its market share to 27.5% following a growth in sales of 8.6%, marking the fifth month in a row that Britain’s largest retailer has made gains.

Lidl is again the fastest growing grocer, boosting sales by 14.1% over the 12 weeks to 26 November to take a record high share of 7.8%. Aldi increased sales by 11.1% and now holds 9.6% of the market. Sales at Asda and Morrisons were up by 2.6% and 3.7% respectively. They now have 13.4% and 8.7% of the market each. Co-op’s share stands at 5.8%, while Waitrose accounts for 4.4% of the market. Frozen specialist Iceland saw an increase in sales of 3%. Growing ahead of the market, Ocado’s sales jumped by 12.1%, holding its market share steady at 1.7%.

*Kantar’s annual Christmas TV ad research conducted using its Link+ creative development tool via Kantar Marketplace. Kantar asked 3,600 UK consumers what they thought about 25 of this year’s Christmas ads and compared the results to the world’s largest advertising database.