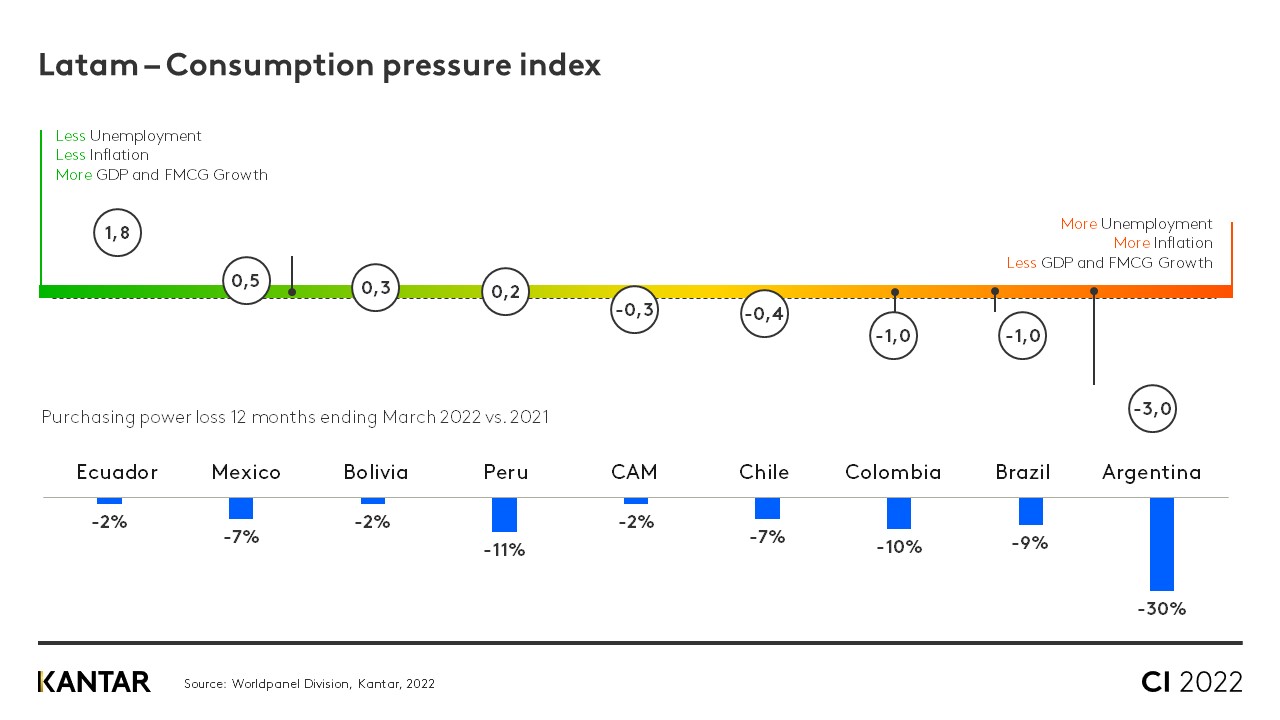

1. FMCG gains in importance within a difficult context

The conflict in Ukraine has increased inflation that was already high in Latam, leading to an immediate response from consumers: to reduce the volume of goods and products they buy. By April 2022, rising inflation had reduced Latin shoppers’ purchasing power by 20% year-on-year. As a consequence, they are prioritising FMCG over other purchases, and this sector is where the biggest opportunities for brands can be found. FMCG’s share of household spending has now reached 37%, rising to 41% in households with children.

Consumers are finding the situation more favourable in countries where unemployment and inflation are below the regional average, such as Ecuador, Mexico and Bolivia.

2. OOH consumption has not yet managed to recover

Out-of-Home spending is still 15% below pre-COVID-19 levels, while In-Home has increased by 25%. OOH consumption had been recovering following lockdowns, but the relaxing of social restrictions was not enough to fuel a sustained recovery. The sharp rise in prices has limited household budgets, and habits acquired during the pandemic persist, such as cautiousness around consuming outside the home, due to official health measures and economic constraints. As a result, OOH has once again lost relevance in the mix.

3. Each trip counts – and the shopper is omnichannel

People are visiting the point of sale less and less often, keeping shopping frequency lower than it was in 2019. This means there are 1.3 million fewer occasions available to target compared to pre-pandemic times.

In parallel with this trend, shoppers increased the number of channels they visited by one on average – a rise of 10% compared with Q2 of 2019 – in a quest to maximise their spend.

Almost 80% of the FMCG growth in Latam now comes from omnichannel shoppers, who visit eight or more channels. This group of consumers is made up mainly of medium and high socio-economic groups, and bigger families with three or four members.

This is the new reality: a fragmented channel landscape, with consumers visiting points of sale less frequently and spending less.

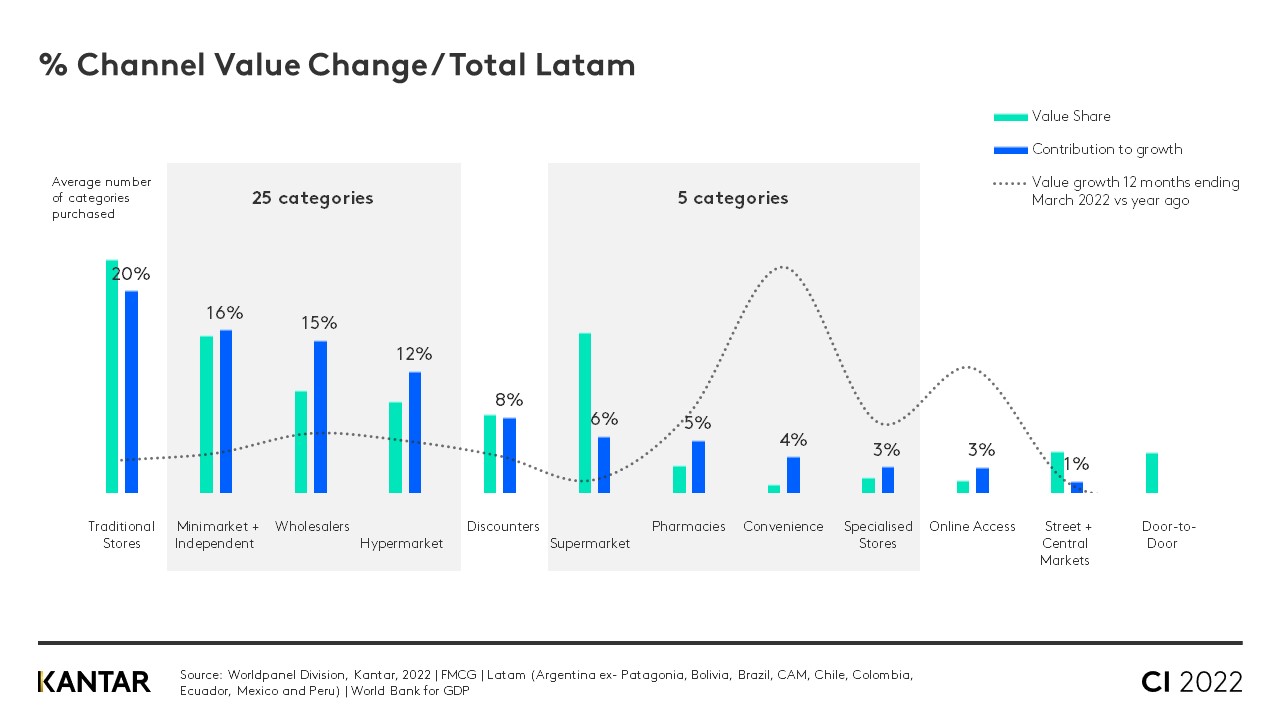

4. Winning channels help shoppers buy more for less and address specific needs

Channels that offer proximity and value-for-money continue to do best in Latam. The contribution made by wholesalers to FMCG growth remains 50% higher than the channel’s relative ‘weight’ in terms of total spend: while it represents 10% of overall FMCG spending in the past 12 months it’s responsible for 15% of the growth. Penetration is the main driver, as consumers are rationalising the volume they buy and the spend for each trip.

Specialised stores, pharmacies, online platforms and convenience stores are the standout performers – the latter making a growth contribution four times higher than its ‘weight’ within the channel mix – driven by more shoppers making bigger purchases.

In addition to gaining new buyers, convenience stores have conquered the challenge of rising expenditure: people are willing to spend more per item when they’re only buying a few items, as it has a smaller impact on the household budget.

Each channel has its own strengths. Those that shoppers visit for stock-up missions provide an assortment and prices better suited to larger purchases, while those addressing specific needs offer more focused missions and promotions.

5. Online grows, but at a slower pace

The percentage of Latam households buying FMCG online has stabilised at 24%. Although it continues to grow rapidly, ecommerce is no longer the channel that has developed the most in absolute terms: convenience stores have exceeded its growth in the last year.

While online penetration has increased ninefold since 2019, purchase frequency has only grown by 13%. Average value sales growth also lags behind the rise in penetration. Strategies that will improve the shopper experience, and drive up frequency of use and loyalty, will now be key to elevating online performance in the region.

Our team understands the macroeconomic situation in each country within Latin America, and can help you maintain your brand’s presence during the slowdown by designing the right strategy for each channel. Talk to our experts now.