Grocery price inflation rose by 17.3% in the four weeks to 16 April 2023, down marginally on the 17.5% recorded in the previous four weeks according to our latest data. Take home grocery sales grew by 8.1% over the month to mid-April.

The latest drop in grocery price inflation will be welcome news for shoppers but it’s too early to call the top. We’ve been here before when the rate fell at the end of 2022, only for it to rise again over the first quarter of this year. We think grocery inflation will come down soon, but that’s because we’ll start to measure it against the high rates seen last year. It’s important to remember, of course, that falling grocery inflation doesn’t mean lower prices, it just means prices aren’t increasing as quickly.

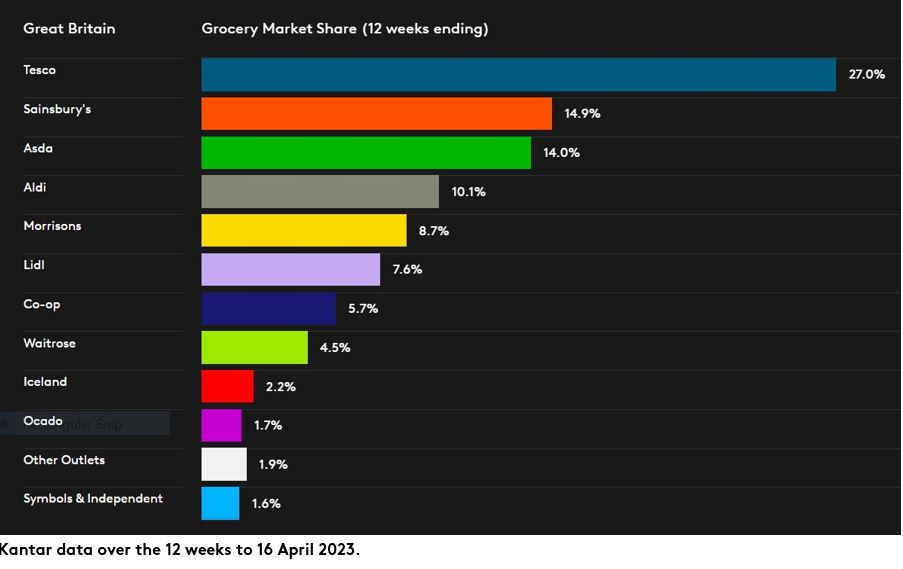

Shoppers trade down while Aldi reaches double digit share

After ten months of double-digit price growth, the British public is continuing to turn to own label lines to help manage spending. Own label lines, which are often cheaper, are still growing at 13.5% this period suggesting shoppers are finding better value for money on these shelves. The very cheapest value own label lines are doing even better, with sales soaring by 46% versus a year ago. These products now find their way into nearly one in five baskets. Branded sales are going up but more slowly at 4.4%.

Amid rising prices, both Aldi and Lidl hit new record market shares over the latest 12-week period at 10.1% and 7.6% respectively. Lidl was the fastest growing grocer with sales increasing by 25.1%, while Aldi is just behind on 25.0%. Consumers are continuing to shop around, visiting at least three major retailers every month on average. The discounters have been big beneficiaries of this, with Aldi going past a 10% market share for the first time this month. That’s up from 5% eight years ago in 2015, so we can see just how competitive the market can be. Retailers are really battling it out to show value to shoppers, but if consumers feel their offer isn’t quite right then they’ll go elsewhere.

Nation indulged in Easter treats

Shoppers embraced the Easter spirit this April despite ongoing pressure on their household budgets. It was a record-setting Easter, with a whopping 38 million chocolate eggs and treats bought in the week running up to Easter Sunday, five million more than last year. Households on average spent nearly £14 on Easter chocolate over the month, which works out at around six packs on average. People didn't hold back on other favourites either; the number of hot cross bun packs sold nudged up by 5% while 3.4 million households picked up a lamb joint for the traditional seasonal roast during the four weeks.

Shoppers are likely to be looking ahead to the three bank holidays in May, including for the Coronation, which could impact grocery sales. We’ve recorded bumps in supermarket sales for previous major royal events. During the week of the Platinum Jubilee last year, they were £87 million higher than the average in 2022. We’ll be keeping a close eye on the data in the weeks to come to see if we get the same effect this time around, including how many of us indulge in a Coronation Quiche. Only half of British households bought a quiche over the past year so it might not be for everyone.

The three largest grocers continued to grow at similar rates in the 12 weeks to 16 April 2023. Asda led the pack with sales up 8.8% year on year, giving the retailer a 14.0% share of the market. Tesco and Sainsbury’s weren’t far behind with their sales increasing by 8.0% and 8.7%, claiming 27.0% and 14.9% of the sector respectively.

Morrisons’ sales continued to increase, and it now holds an 8.7% share of the market. Co-op’s market share stands at 5.7%, with sales growing by 2.7% in the latest 12 weeks. Waitrose’s sales increased by 3.2%, its best performance since June 2021, pushing its market share to 4.5%. Iceland matched the 12-week market growth rate of 9.4%, maintaining its level of share at 2.2%. Ocado outpaced the overall online market, increasing sales by 8.7%.