In the midst of a strict lockdown in Shanghai, as well as the emergence of COVID-19 cases in Beijing and a few other cities, the FMCG market in Mainland China grew by 1.5% year-on-year over the 12 weeks to 22 May 2022. Consumers stocked up on food categories, whilst cutting back on beverage and personal care products.

Although the lockdown and reduced mobility tilted demand toward stock-up buying, the shockwaves in key cities was not offset by more ‘home-based’ consumption. This resulted in a 0.8% year-on-year decline in FMCG sales value in key cities over the past 12 weeks. In contrast, during the same time period, provincial capital cities and prefecture level cities continued to report strong value growth of 2.1% and 3.2% respectively.

Hypermarkets hit as consumers shop smaller

Modern trade value grew 2.1% over the latest 12 weeks compared with the same period last year, driven by the strong performance of smaller supermarkets and convenience stores, whereas hypermarkets saw a 3.2% drop in FMCG value sales.

Amongst the key players, Sunart group reported an 8.9% fall in sales as its store portfolio in the East region was more severely impacted by the forced closures. Yonghui, which focuses more on the West and South regions, reported moderate growth of 4.7%. Walmart group continued to race ahead with 7.8% growth, thanks primarily to the strong gains made by the members’ only Sam’s Club.

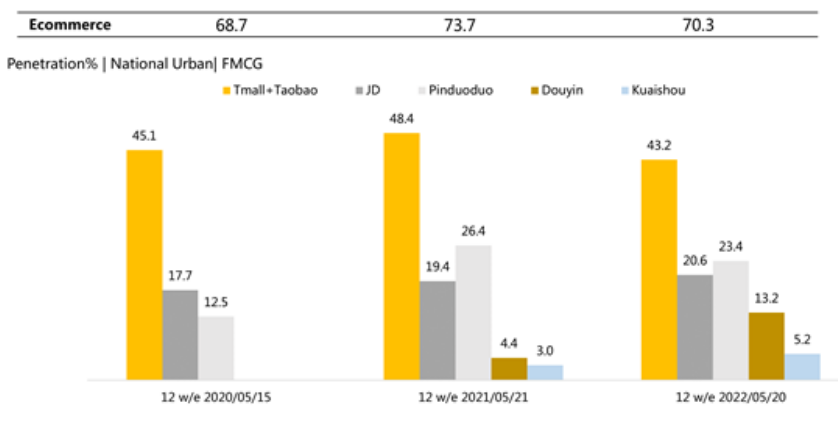

Ecommerce growth is steady

The ecommerce channel witnessed a moderate value growth of 1.4% for the latest 12 weeks, and 3.9% growth in the four weeks to May 22. JD continued to lead the way, with an increase of 4.8% in FMCG spend and a steady year-on-year penetration lift of 1.2%. Alibaba and Pinduoduo maintained their market share and penetration.

The short video platforms Douyin (TikTok) and Kuaishou managed to gain additional penetration of 4.7% and 1.3% respectively in May, capitalising on the increased consumption of short video content during the lockdown period.

Source: Kantar Worldpanel, 12 weeks to May 2022

With transport restrictions affecting the delivery of FMCG products by mainstream ecommerce players, online-to-offline (O2O) commerce saw further increases in penetration. Community Group Buy, Aggregator, and frontline fulfilment-based delivery companies all posted outstanding performances in May, with 34.7% of Chinese families using O2O to shop for groceries in the latest 12 week period.

Please contact our experts for more information on the evolving FMCG market in Mainland China and access our data visualisation tool to explore current and historical grocery market data for your region.